A joint AGN & Nexia thought-leadership publication, developed through global collaboration at the AGN & Nexia World Congress, Munich.

This Global Business Voice draws on the insights gathered during the Future Funding workshop delivered at the AGN & Nexia World Congress in Munich in late 2025. Partners from AGN and Nexia member firms across Europe, the Americas, Asia-Pacific and emerging markets explored how accounting firms are responding to accelerating structural change, new capital and funding models, and new sets of tech enabled well-funded competitors.

Tune into our mini podcast on Spotify for a quick summary of the key insights.

A Clear Message is Emerging

Across this research, a clear message is emerging: the future of the accountancy profession will be shaped less by access to capital itself, and more by how deliberately firms align capital with capability, culture and career pathways. Insights from the joint AGN and Nexia World Congress in Munich do not point to a single dominant funding model, but instead reveal a profession becoming more reflective, more strategically literate and more aware of trade-offs—balancing growth with autonomy, scale with culture, and speed with long term sustainability.

What emerged was not a single answer, but a revealing pattern of shared pressures, divergent strategies and unresolved tensions—all of which merit closer examination.

The session combined:

- AGN workshop material on funding models, consolidation and professional impact

- Case examples from multiple jurisdictions

- Personal and group worksheet responses to a range of questions.

- Snap Mentimeter workshop polls on a range of related questions.

Key themes

The analysis of the workshop presents a series of important recommendations and observations drawn from the lived experience of our own members:

- Global dialogue accelerates strategic learning – The consistency of themes across geographies reinforces the value of AGN–Nexia collaboration.

- Funding and talent strategies are converging – Ownership and incentive models are now evaluated as much for people impact as for capital efficiency.

- Scale and independence are no longer binary choices – Firms are exploring ways to access scale benefits while retaining identity and autonomy.

- The profession is in a design phase – Firms are increasingly designing ownership, governance and career models rather than inheriting them

1. Digging Deep Into The Delegate Worksheet Responses

1.1. Structural, Not Cyclical Change

Personal Worksheet Question 1:

“Do you believe the competitive environment for accounting firms is changing? If so, how?”

The question deliberately left room for interpretation, which is reflected in the breadth of responses. The answer is a big ‘YES’ and below the delegates feedback the major factors that have changed.

The five dominant themes that emerge from the delegate personal worksheet responses…

Technology and AI are the primary competitive disruptor

Competitive pressure as being primarily driven by:

- AI adoption & automation

- Cost compression in compliance work

These responses typically link technology to:

- Increased efficiency expectations

- Margin pressure on traditional services

- A shift away from pure compliance toward higher-value advisor

A near universal acceptance that technology is no longer optional but existential.

New funding fuel consolidation & scale threats

Many respondents describe:

- Accelerating consolidation

- Growth of larger, better-funded firms

- Competitive advantage created by access to capital

Importantly, while private equity is frequently mentioned, it is usually framed as an enabler of scale and technology, rather than as a threat in isolation.

Talent scarcity and changing people dynamics

Respondents frequently highlight:

- Talent wars & skills gaps (particularly digital and advisory)

- Retention challenges

- Changing expectations of younger professionals

Several answers link talent directly to funding, noting that:

- Capital is required to attract, retain, and motivate staff

- Traditional partnership models struggle to compete with funded firms on career propositions

Market polarisation and service model shift

A subset of respondents articulate a more nuanced view:

- Markets splitting between scaled, cost-driven platforms and high touch advisory firms

- Compliance becoming commoditised

- Value migrating toward advisory, ESG, and specialist services

These answers tend to be more reflective and strategic, indicating respondents thinking beyond immediate competitive pressure to long-term positioning choices.

Regional variation and uneven pace of change

Some respondents explicitly note that:

- Competitive pressure varies significantly by country

- Smaller economies or regulated markets feel change more slowly

- Global narratives do not always map cleanly onto local reality

This theme provides an important counterbalance to more universal claims and reinforces the workshop’s emphasis on jurisdiction-specific strategy.

“The profession is consolidating, and firms

with access to capital are able to invest faster

in technology and people.”

AGN member firm – Sweden

“AI and automation are pushing compliance work into a cost-driven space.”

Nexia firm – United Kingdom

Q1 Conclusions

The near absence of dissent suggests a mindset shift: competition is now widely perceived as structural rather than cyclical. Once this threshold is crossed, firms tend to reassess ownership, capital and long-term positioning far more seriously. Very few respondents challenge the premise of increased competition, reinforcing the perception of structural change as widely accepted.

The problem definition is widely accepted: firms feel under pressure.

The solution space is still forming: funding models are seen as enablers, not answers in themselves.

There is strong appetite amongst members for:

- Comparative funding insight

- Case-based learning

- Guidance on balancing scale with culture and career value

The topic should continue to be framed, not as a binary PE vs non-PE decision, but as a strategic tool kit aligned to market position, geography, and long-term professional values.

2. Strategic Priorities Ranking – Technology No 1 but coupled with talent

Personal Worksheet Question 2:

“What are the main strategic priorities your firm needs to focus on?”

Q2 responses represent a clear transition from environmental diagnosis (Q1) to internal action and strategic intent. Compared with Q1, answers are more pragmatic, firm-centric, and operational.

Five dominant themes emerge from the personal worksheet responses with strong overlap between them.

Technology investment and digital transformation

Most frequently cited theme

The majority of respondents identify technology as a core strategic priority, typically expressed as:

- Investment in AI, automation and digital tools

- Modernisation of IT stacks and systems

- Process efficiency and scalability

Technology is rarely framed as experimental. Instead, it is treated as foundational infrastructure required to remain competitive.

Typical framing includes:

- “Investment in AI and IT tools”

- “Digital transformation”

- “Prioritising the IT stack”

Notably, respondents often link technology directly to productivity, margin protection and future scalability rather than innovation for its own sake.

Talent development, retention and motivation

Second most common theme, closely coupled with technology

Talent emerges as a strategic priority almost as frequently as technology, but with a different emphasis:

- Retention of skilled staff

- Development of new skills (especially digital and advisory)

- Motivation, engagement and career progression

Several responses explicitly connect talent strategy to funding, implying that access to capital is necessary to support training, incentives and competitive career propositions.

Talent is not framed as a short term recruitment problem, but as a structural capability issue.

Service evolution and client value proposition

Moderate frequency, higher strategic maturity

A significant subset of responses focuses on:

- Clarifying or evolving the firm’s value proposition

- Shifting towards advisory or higher-value services

- Being more client-centric rather than service-led

These responses often reflect a recognition that:

- Compliance services are under margin pressure

- Differentiation must come from service mix, insight and relationships

This theme is less common than technology or talent, but where it appears, it tends to be more strategically articulated.

Process, structure and organisational readiness

Operational but strategically important

Some respondents emphasise:

- Developing internal processes

- Organisational robustness

- Readiness for growth, transformation or external capital

This theme is frequently paired with technology investment and reflects concern about execution capability rather than vision alone.

Culture and professional identity

Lower frequency but conceptually significant

A smaller number of responses explicitly reference:

- Cultural continuity

- Maintaining “human” elements of the profession

- Balancing change with professional values

Although less frequently mentioned, this theme is important contextually, particularly when read alongside Q4 (future concerns).

Q2 Conclusions – Technology and talent are tightly coupled

One of the strongest patterns in Q2 is how often technology and talent are mentioned together. Respondents implicitly acknowledge that:

- Technology investment without skills will not deliver value

- Talent without modern tools is constrained

This reinforces the Future Funding Munich course message that capital must translate into capability, not just infrastructure.

Emphasis on readiness rather than growth – Very few respondents list “growth” as a primary strategic priority. Instead, they focus on:

- Readiness to transform

- Capability to adapt

- Sustainability of current operating models

Question 2 reveals a profession less focused on choosing a funding model, and more focused on ensuring it has the capability to execute whatever strategy it ultimately chooses. Technology and talent dominate strategic priorities, with service evolution and organisational readiness acting as supporting pillars. Cultural considerations appear less frequently, but signal deeper concern about the long-term implications of rapid change.

3. Funding Models – Maintain control and mix it up

Personal Worksheet Question 3:

“What funding models are you considering or currently using?”

Q3 responses move from what firms need to do (Q2) to how they believe those priorities can realistically be funded. Compared with Q1 and Q2, the tone of responses is notably pragmatic and non-ideological.

Rather than advocating a single preferred funding route, most respondents describe options, combinations, and trade-offs.

Five dominant themes emerge – Personal Worksheet Responses

Hybrid and blended funding models

Most frequently cited response type

The single strongest signal from Q3 is the prevalence of hybrid thinking. Many respondents explicitly reference:

- Combinations of partner capital, bank debt and external funding

- Using different funding tools for different strategic objectives

- Avoiding over-reliance on a single capital source

Typical language includes:

- “A mix of…”

- “Blended approach”

- “Combination of debt and equity”

This reflects a shift away from viewing funding models as mutually exclusive choices, and towards seeing them as modular and situational.

ESOPs and employee ownership structures

Strong thematic presence

Employee Stock Ownership Plans (or equivalent internal ownership mechanisms) appear frequently, often

framed as:

- A tool for talent retention and motivation

- A means of preserving culture and continuity

- A partial alternative to full external ownership

ESOPs are rarely presented as a pure funding solution in isolation. Instead, they are typically positioned as part of a broader ownership and incentive strategy, sometimes alongside external capital.

Private equity

Widely referenced, but cautiously framed

Private equity is mentioned by a substantial proportion of respondents, but the framing is generally measured rather than promotional. Common characteristics of PE-related responses include:

- Recognition of PE as a source of scale and capital

- Awareness of time horizons and return expectations

- Consideration of governance and cultural implications

Importantly, very few responses frame PE as an “all-or-nothing” proposition. It is more often discussed as:

- One option among several

- Potentially suitable for some firms or phases, but not all

This aligns closely with the neutral treatment of PE in the Future Funding Munich course material.

Traditional partner capital and bank debt

Still relevant, but increasingly constrained

Traditional funding routes remain part of the conversation, including:

- Partner equity contributions

- Retained profits

- Bank lending

However, these options are often described as:

- Insufficient on their own for major technology investment

- Limited in their ability to support rapid transformation

Several respondents imply that traditional models work best when augmented, rather than relied upon exclusively.

IPO or public market options

Low frequency, niche relevance

Initial Public Offerings or public market routes are mentioned only rarely. Where they do appear, they are

generally:

- A long-term or theoretical option

- Relevant only for a very small subset of firms

This suggests that, at least among workshop participants, IPOs are seen as exceptional rather than mainstream funding paths.

Q3 Conclusions – Pragmatism over ideology

One of the most striking features of Q3 is the absence of polarised positions. Respondents rarely argue that one funding model is “right” or “wrong” in principle.

Instead, they focus on:

- Fit with strategy

- Stage of firm development

- Cultural and people implications

- Support succession planning

Question 3 reveals a profession that is becoming more financially literate, more pragmatic, and more strategic in how it thinks about funding. Rather than searching for a dominant model, firms are assembling bespoke funding architectures aligned to their strategy, culture and stage of development. Hybrid approaches, ESOPs and selective use of external capital dominate thinking, while traditional models are increasingly supplemented rather than relied upon alone. As such, Q3 provides the practical counterpart to the strategic priorities identified in Q2 and sets the context for the concerns and uncertainties explored in Q4.

4. The Future is Unclear – Containing Risks and Uncertainties

Personal Worksheet Question 4:

“What concerns or uncertainties do you have about the future?”

Q4 responses are qualitatively different from Q1–Q3. Where earlier questions focus on diagnosis, priorities and options, Q4 exposes underlying unease, ambiguity and unresolved tension. Fewer respondents answer Q4 in detail, but those who do tend to express deeper strategic and professional anxieties.

Five dominant themes emerge – Personal Worksheet Responses

Uncertainty about end-states and “what happens next”

Most frequently expressed concern

The most common concern is not about immediate competition or funding mechanics, but about long term outcomes:

- What does the profession look like after consolidation?

- What happens after PE investment or second-round “flips”?

- Where do current strategies ultimately lead?

Typical expressions include:

- “Too soon to know”

- “What is the end game?”

- “What does the market look like after this wave?”

This uncertainty is often expressed without proposing solutions, indicating that respondents see this as a systemic unknown, not a problem that can be managed internally.

Technology pace versus firm readiness

Second most common theme

Many respondents express concern not about whether AI and digital transformation will occur, but about preparedness:

- Are firms investing in the right technology?

- Are people ready to use it effectively?

- Will technology outpace training, governance and culture?

Technology appears here less as opportunity and more as execution risk. This concern is particularly notable given that technology dominates Q2 priorities—suggesting a gap between aspiration and confidence.

Culture, identity and professional values

Moderate frequency, high significance

A number of responses raise concerns about:

- Loss of firm culture during rapid growth

- Erosion of professional identity

- The impact of commercial pressure on traditional values

Although fewer in number, these responses tend to be more reflective and emotive, pointing to deeper anxieties about the nature of the profession itself, not just business models.

Talent pathways, skills and career sustainability

Moderate frequency

Some respondents express concern about:

- How to develop skills in a rapidly changing environment

- Whether future career paths remain attractive or credible

- Succession planning in a transformed ownership landscape

These concerns often link back implicitly to funding and ownership models, particularly where traditional partnership pathways are perceived to be narrowing.

Market and regulatory uncertainty

Lower frequency, contextual concern

A smaller subset references:

- Regulatory responses to consolidation or AI

- Market reactions to funding structures

- Jurisdiction-specific uncertainty

While less prominent overall, these concerns reinforce the sense that external forces remain unpredictable.

Q4 Conclusions – Strategic optionality over certainty

Workshop delegates are not expressing fear so much as acknowledging ambiguity. Results of Q4 highlights a tension – the need to move quickly (technology, consolidation, funding), versus the need to preserve culture, people and professional standards. This tension remains an open strategic question for many firms.

Question 4 reveals a profession that is strategically active, but consciously uncertain about its long-term destination. The dominant concern is not competition or access to capital, but what the profession becomes after the current wave of consolidation, technology adoption and funding innovation plays out. Technology readiness, cultural continuity and talent sustainability emerge as key fault lines, while many respondents explicitly acknowledge that it is “too soon to know” how these forces will ultimately resolve.

Conclusion: funding the firm, shaping the profession

This GBV reinforces a message emerging consistently across AGN and Nexia research.

The future of the profession will be shaped less by access to capital, and more by how deliberately firms align capital with capability, culture and career.

Insights from the AGN & Nexia World Congress in Munich do not point to a single dominant funding model. Instead, they reveal a profession that is:

- More reflective

- More strategically literate

- More aware of trade-offs

As a joint AGN and Nexia publication, this GBV demonstrates the value of shared global insight—not as a source of answers, but as a framework for better questions.

Top Line Member Firm Takeaways

Treat funding as a strategic design choice, not a binary decision – Hybrid and blended funding approaches are increasingly common and may offer greater flexibility than single-model solutions.

Align capital strategy explicitly with talent strategy – Ownership structures, incentive models and funding horizons are now central to recruitment, retention and succession.

Invest in technology with clear strategic intent – AI and automation amplify strategy; without a clear service and client proposition, investment risks commoditisation rather than differentiation.

Preserve flexibility in an uncertain market – Firms are increasingly valuing reversibility and flexibility over speed alone, particularly in ownership and governance decisions.

Use international collaboration to accelerate strategic learning – Global peer dialogue, such as that enabled through AGN and Nexia platforms, is becoming a material advantage in navigating change.

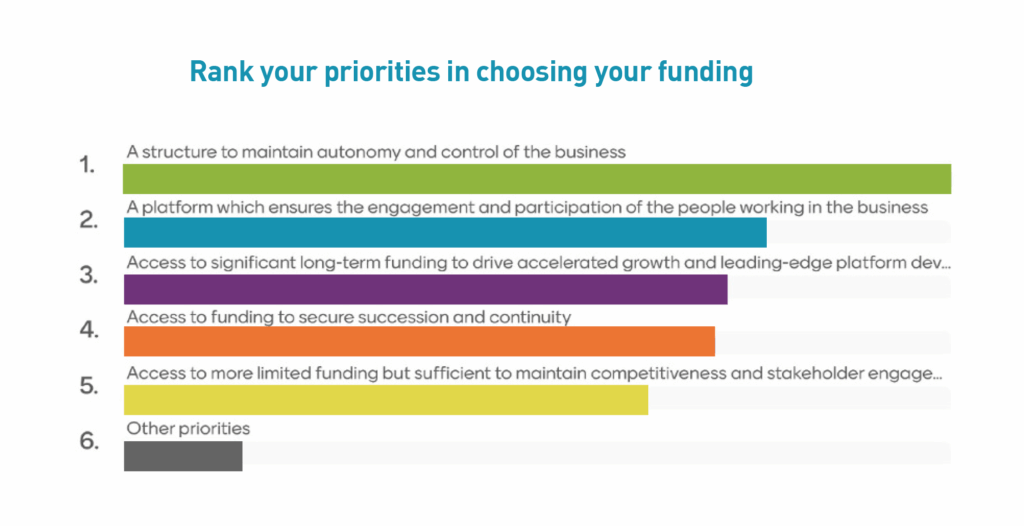

Appendix A: Snapshot Audience Polling Responses

Throughout the 3hr workshop session, we complemented the individual worksheet responses and table responses with a running audience poll of some of the key issues raised in the future funding debate.

SNAPSHOT MENTIMETER POLLING RESPONSE

The highest-ranked priority is maintaining autonomy and control, followed by engagement and participation of people within the business. Access to long-term growth capital ranks below these human and governance factors. Pure growth capital, without reference to people or control, is not the primary driver.

This slide provides strong empirical reinforcement for one of the paper’s most important insights: funding decisions are now inseparable from talent, culture and governance considerations.

It validates the repeated observation that capital is viewed as an enabler, not an end in itself, and that ownership structures are being evaluated through a people and career lens.

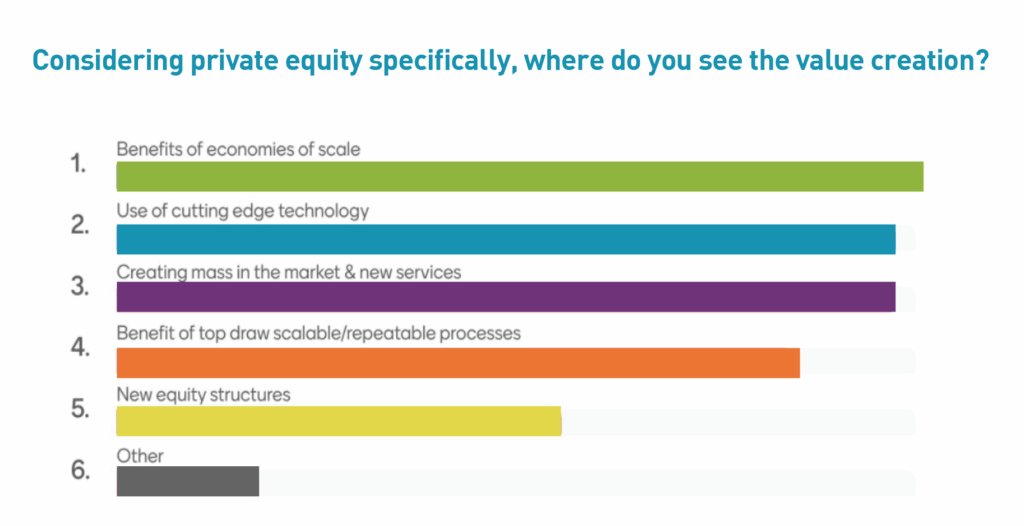

Delegates associate PE value primarily with scale, technology investment, new services and scalable processes. “New equity structures” rank lower, indicating that financial engineering itself is not perceived as the main value driver. The value narrative is operational and strategic, not transactional. This slide supports the paper’s deliberately neutral treatment of PE. It shows that delegates do not see PE as value-creating because it is PE, but because of what it can enable: investment, scale and execution capability.

Useful AGN Reference Materials:

- The Future of Accounting – Insights from AGN NextGenners

- The Pace of Digital Transformation vs Client Readiness

- Evaluating AGN Member Digital Maturity

- The AGN Digital Maturity Diagnostic Tool

- Unleashing the Power of ChatGPT

For further information on this topic or anything relating to the AGN International Association of Accounting and Advisory Firms or to become an AGN member, please email your closest AGN Regional Director (see below) or go directly to www.agn.org.

Malcolm Ward

CEO AGN International

[email protected]

Robert Zhang

APAC Representative

[email protected]

Marlijn Lawson

EMEA Regional Director

[email protected]

Christian Moises

Americas Regional Director

[email protected]

Copyright © 2026 AGN International Ltd. All rights reserved. No part of this publication may be reproduced, distributed, or transmitted by non-members without prior permission of AGN International Ltd.