AGN Global Business Voice: International Business Issues

Are you interested in a valuable proposal?

Almost every week, many accounting businesses are getting “those calls“ related to business value. In some respects, it’s really nothing new. Larger firms have absorbed smaller ones for many decades, and from time to time, we have seen externally funded consolidators active in the market. It’s certainly the experience in the US and Europe and parts of Asia that famous accountancy brands, regional or local, have been absorbed into larger internationally branded firms or even into technology businesses. (Read our June 2022 AGN Global Business Voice – The New Consolidators?)

But could it be different this time? Certainly, the pandemic has catalyzed a number of trends that have been brewing for a long time. And now it would appear that business valuations are at an all-time high. Tempted? Inevitably, every situation has “a number”, but it could equally be that the offer is not there, and neither is a clear path for the next generation. You need to realize the value you have generated in your firm for your own future. What to do?

In this Global Business Voice, we take a look at the present environment for valuations, unpicking some of the key features and trends, and then suggest some practical steps that AGN members can take to maximize their position – Develop and realize business value. The author draws experience mainly from the US and Europe, and it’s accepted that the situation may vary in different regions across the globe.

Establishing ‘Business Value’ has never been straightforward.

Compared to a business, for example, with a substantial asset base or a unique proprietary process, “value” in professional services is traditionally considered ephemeral. This is because it depends on the retention and motivation of talented individuals (who can only be secured to a limited extent), delivering to well-informed and demanding customers complex intellectual property that is hard to differentiate from competitors. Right now, like never before, the industry is subject to dynamic change, fuelled by revolutions in technology, the requirements of human talent and, most recently, flows of new capital.

Historically, activity in the sector was driven by those working in it rather than external professional investors. Both valuations and deals depended on somebody, usually a senior partner in a larger firm, looking at a target and deciding, “Is this opportunity going to give me and my partners a better living, and will it build our coverage and reputation?”.

Why a multiple of revenue?

As far as valuation itself was concerned, features like profitability rates and future cash flows were always obscured by the intimate and complex financial and other arrangements of the owners working in the business. That’s what drove the approach of valuation based on revenue and, in particular, revenue expected to recur annually.

A benchmark multiple of 1 x revenue was often considered a starting point, often with an adjustment for net assets. In reality, perhaps a multiple in the range of 0.6 and 1.3 describes the historic situation more accurately. But it was still merely a proxy to estimate future profit and cash flows. Where in the multiple range you landed could vary widely, depending on gross margin rates, growth prospects, the proportion of recurring to non-recurring fees, cost base and overheads, and a multitude of other factors. But all in all, you were probably ending up with a valuation of somewhere between 3 and 4 times annual net earnings (EBITDA).

At its heart, the traditional approach revolves around the conventions of a “profession” – a business dependent on complicated and risky technical judgments from highly experienced and skilled people who were themselves working in that business. It was primarily an internal view about “practising the craft” of accounting and making a good living as an equity partner. Arguably, it’s the direct opposite of the view of an external professional investor.

External professional investors – a different mindset in a sector that’s changed

Many AGN members can testify that there is a very different approach employed by the present crop of external professional investors. And often that can lead to a seemingly lucrative offer and a higher order of magnitude than we have seen historically.

External professional investors regard the sector as a highly profitable, cash-generative, and low-risk business. The questions in the mind of these investors do not concern their own careers and daily working lives in the business but are about maximizing value and minimizing timescales: “Can I hike rates of profitability in this model by using technology or increasing team leverage/gearing? Or better yet, both. Can I scale up the model by acquiring market share? Can I drive growth by cross-selling new services?”

The attitude is summarised by the reported comment of some investors that they “are not a pension fund for partners at the end of their careers”. It’s a substantially different mindset – and at the moment, it leads to higher valuations, and particularly if the target firm has a strong niche focus, technology that can be leveraged, or is on an attractive growth path. And, of course, none of this is wrong; it’s just a different approach.

So what’s changed to make “the professional craft” into just another business investment opportunity? Undoubtedly, the demographic wave of equity owners looking for retirement is a significant factor. There is also the perception of uncertainty about whether a new generation of professionals is prepared to invest and wait for advancement in the same way as the present crop of equity owners did. But perhaps the mega-trend here is technology, with ever-increasing capabilities and ever-lowering barriers of entry. The pandemic probably accelerated all these factors, and also provided “proof of concept” for new ways of working, and demonstrated that clients will accept them.

An external professional investor’s approach to business value

Historic external professional investment forays into the sector have frequently been unsuccessful. Some suggest that (in the UK at least) the present mindset and new momentum can be traced back to 2016 and Azets, who originated as the accounting division of the Visma Group, a Norwegian-based technology and services company. Backed by private equity and driven by a vision to establish itself as a pan-European mid-market accounting powerhouse, in 2016, they acquired the UK firm of Baker Tilly and went on to acquire and integrate some 90 accounting firms across Europe. They now have around 7,600 professionals servicing more than 93,000 clients, generating approximately £700 million in revenues.

By leveraging advanced digital tools and automation, Azets planned to deliver efficient and streamlined accounting services, enhancing client satisfaction and operational effectiveness while maximizing the profit opportunity. Is it for real?

Well, in June 2023, the original private equity backers of Azets (Hg) took in a co-lead investor (PAI Partners) – the deal terms were not made public, but earlier in the year, there was city speculation of an overall valuation of between $1 billion and $1.5 billion1. So, just for old-time’s sake, that’s probably somewhere around 1.5 times current gross revenues (or around two times, based on the last reported numbers).

But in this, and most transactions in the sector now, multiples of revenue are not so much used, and earnings before interest, taxation, depreciation and amortization (EBITDA) are the focus. And if historically the sector was achieving 3 or 4 times EBITDA, the talk now is of a rising trend of anywhere between 5 and 10. Indeed, we are aware of one deal where the gross revenue multiplier would probably be around 2.5 times, which pretty much equates to the top of that EBITDA range. And perhaps there could be further to go. In the technology sector, multiples of EBITDA have reached levels of 12 or 14 times. There can be little doubt that the race to embrace technology has significantly driven these attractive valuations and gives some indication of how markets value the future prospects of that sector—yet another reason for firms to invest in technology and get up to speed with digital transformation.

Prices can’t keep rising – can they?

Market valuations are historically high and may perhaps have further to rise. But it is worth making note of some cautionary observations:

- The legal sector has five players in the Magic Circle. Right now, the top tier of accountancy has the Big 4 (or 6?), management consultancy 10, probably 4 to 6 global actuaries. So for the mid-tier/SME, focused accounting and advisory business, at what point do we reach market saturation? Whether you view markets locally, nationally or globally, it seems clear that demand will not support an unlimited number of successful players. And, of course, external professional investors know it – approaching a perceived point of market saturation will have a knock-on negative effect on values.

- There is a huge assumption here that technology developments deliver economies, efficiencies (and new services), and support the strategy to aggregate firms. But, on the contrary, might technology also drive fragmentation? Artificial intelligence technologies became useful and ubiquitous very quickly (ChatGPT – 4 months). We’ve also seen powerful innovations tend to come from start-ups, individuals, and small businesses. For example, in the UK, surely technology has helped drive the 40% increase in small independent practices and bookkeepers, increasing from around 55,000 to 77,000 since 2018. Doesn’t this chime with Generation Z’s propensity to reject conventional career patterns, the work-from-home movement, and the current dearth of qualified talent?

- Whatever generational label you care to apply, is it right to assume that upcoming young professionals will accept roles with less annual compensation and less autonomy than the present crop of equity owners, all in exchange for employee shares/options which they hope will one day be worth a lot of money? We comment above on a perception that this new generation of professionals is not prepared to invest and wait for advancement. But does that underestimate the entrepreneurial spirit and desire for relative autonomy, which has always been so attractive to professionals working in smaller firms? Much like technology, there are some big assumptions being made here.

Right now, we could perhaps be living through a golden era for the valuable small and medium-sized firms to cash out. Of course, that cannot and should not be ignored. But so far, at least, accounting and advisory business, at what point do we reach market saturation? Whether you view markets locally, nationally or globally, it seems clear that demand will not support an unlimited number of successful players. And, of course, external professional investors know it – approaching a perceived point of market saturation will have a knock-on negative effect on values.

SOURCES:

https://news.sky.com/story/accountancy-firm-azets-owner-runs-numbers-on-1-5bn-sale-12665320

IRIS Industry analysis Feb 2023

External finance? It’s not for everyone.

In the end, perhaps the realization of ‘value’ of an accounting firm comes down to vision and direction (and their close cousin ‘culture’) – what do the participants in a particular business regard as “valuable”? What type of professionals are you and your firm? Thus, what approach is most likely to deliver your objectives? Below we describe two scenarios, perhaps a little exaggerated for the sake of emphasis. The first may well suit an external investment scenario of the types discussed above. The second, perhaps less so.

SCENARIO 1

Scale, Dynamism & Value Growth

Centred around rapid expansion, service innovation, technology, consolidation, and eventual quick sale to achieve substantial

financial gains for the owners (perhaps an

independent investor) and a capital war chest

for the firm’s future. The primary objective is

to achieve rapid growth by acquiring smaller

accounting firms, integrating their client base,

and expanding the firm’s reach. Efficiency

and scalability are key considerations,

implementation of streamlined processes and

leveraging technology to optimize operations.

It takes good care of its people, mainly through

financial reward rather than other means

Senior-level lateral hires are essential to

development. The primary goal is to build

the firm’s value quickly and position it for a

lucrative sale to another accounting firm, an

investment group, or a larger corporation.

The owners’ aim is to capitalize on the firm’s

market position and profitability to secure a

substantial return on their investment and

move on.

SCENARIO 2

Legacy, Reputation & Client Service

This type of accounting firm vision prioritizes delivering exceptional service for a premium and achieving organic growth over time. The firm aims to build a reputation for developing long-term client relationships and consistently exceeding client expectations. The firm has a culture that is focused on excellence in the longer-term growth and development of its people – it seldom makes senior-level lateral hires. This vision emphasizes organic growth, gradually expanding the client base through referrals and positive word-of-mouth. A merger is a secondary objective, and capital investment will come from new equity partners, reserves, or bank lending. The firm’s goal is to remain independent, build a sustainable and profitable business, ensuring a smooth transition of ownership and leadership through succession planning, enabling them to retire while maintaining the firm’s reputation and commitment to service excellence. Of course, there is a whole spectrum of variants between these two opposite positions. But neither approach is wrong; they are different, and they will beget different strategies and decisions.

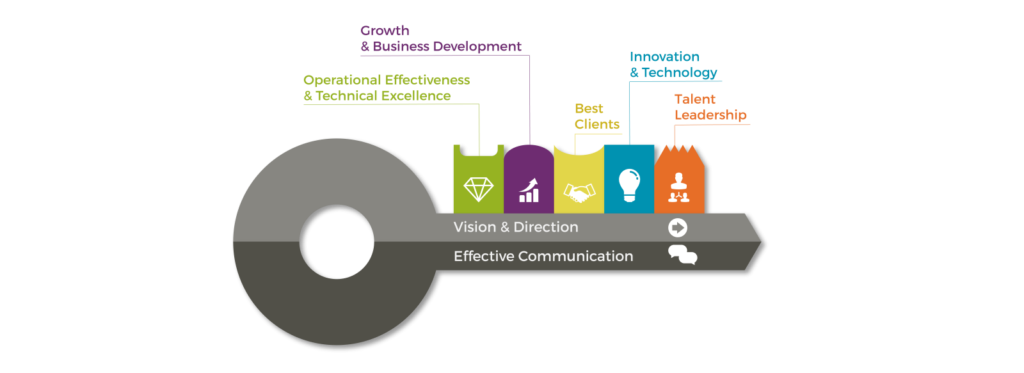

Common vectors of business value – The AGN Value Key

(See Appendix 1 for practical application of the AGN Value Key)

The good news is that the underlying ingredients or vectors of value are the same, regardless of a firm’s vision or culture.

The AGN Value Key is a model that exhibits the enterprise “value elements” that need to be progressed to build enduring value in accounting and advisory businesses. The two scenarios above describe different combinations of the keys to value, with different value elements playing at different volumes or emphases, but they are all encompassed by the AGN Value Key. By identifying, investing in, and developing the correct elements, it is possible to assure the firm for the longer term as a valuable business.

The AGN model identifies and develops the required elements, which we describe below with some suggested key challenges of relevance to many AGN members.

Vision, Direction, and Communication

All of the value elements will require the coordination and direction of effective leaders

who can communicate and project a vision for the business in an engaging and inspiring way. Often these key elements are performed by an entrepreneurial founder (or founders). Particularly when considering robust succession, these key leadership skills should be identified, developed and trained in the same way as technical and business development skills. Vision, direction, and, consequently, strategy are primary ingredients in the organizational amalgam that is culture, and we noted above the critical role culture has to play in determining how you realize value.

Operational Effectiveness and Technical Excellence

The engine room of the business, comprising the four elements bound together by management, fiscal discipline and leadership:

• Customers

• People

• Capabilities

• Reputation

This value element concerns strong performance in the basic functions required to win work and satisfy clients, obtain, retain, and develop talented people, and maintain high technical standards and an appropriate operational footprint while also growing the reputation and visibility of the practice. It’s also imperative to demonstrate a stable and transparent financial control system with accurate, timely reporting and financial forecasting.

Growth & Business Development

This value element concerns the future growth story for this practice – what are the strategies and plans that make us believe tomorrow will have higher revenues and profits than today? Value is achieved by understanding the trends and themes, how they impact the particular business, where the best future opportunities lie, and that you have team members who understand and can pursue these opportunities. An approach embracing environmental, social and governance (ESG) opportunities will be an attractive valuation consideration. Particular value can be found in niche markets and specialisms that can’t easily be replicated by competitors. (Refer to AGN 6 Star Business Development Model at My AGN / AGN Solutions (or My Resources) / Business Strategy & Growth).

Best Clients

Which clients contribute best to the strategy of the business? Whether it be revenue,

profitability, reputation, or developing technical

credentials, often the 80:20 rule applies – certain

clients are disproportionately beneficial – Crown Jewel or key accounts. How are they contracted? Can you demonstrate stable future income from them and ideally develop strategies to increase

that income? Are you using periodic independent

reviews of performance and satisfaction and identifying strategies to maximize your share of the wallet by providing valuable services?

Innovation & Technology

The current and potential future impacts of technology are so pervasive in business

performance, an evolved and articulated approach to the area is essential. It is clear that an approach to the future of technology is both a key business performance driver and a driver of external valuation criteria. A credible approach to digital transformation will require a deeply informed and relevant understanding of the impacts on both the service offer, client demand, and operations of the business, along with expected timelines, skills requirements, and resources.

Talent Leadership

In the context of the current global war for talent, you need to demonstrate effective approaches to recruitment, retention, and development of talented people who have a deep engagement and belief in the future of the business. This not only drives performance, but resilience, succession, and, therefore, value.

In Conclusion – a bubble of opportunity?

Some lucrative opportunities exist to crystallize value because external investors are taking a different perspective of the sector. Unlike many historic investors, there is no consideration of their own careers working within the business. Instead, they perceive a low-risk, high-profit, cash-generative opportunity purely from an investment perspective. They believe that market share can be accumulated in a fragmented competitive landscape with an ownership demographic looking for an exit. Their view is that profitability and growth can be supercharged by leveraging technology, economies of scale, cross-selling new services, and returns on investment can be focused on a narrower pool of equity participation.

A fundamentally different view of the business is being taken, which is being used to justify valuations at two or three times historical levels. Presumably, this will either prove justified or unravel in the coming years, but either way, we could presently be in a golden age for the valuation of small and medium-sized

accounting advisory businesses. How long any “valuation bubble” will sustain is, of course, impossible to say. And indeed, perhaps it has further to inflate, especially when the FinTech sector is considered. In the meantime, high-performance and top valuations are, in our experience, being driven by businesses with an evolved plan for technology and the opportunities around ESG. This needs to be supported by a skill/talent plan, which not only meets these needs but drives resilience and succession.

But inevitably, markets for SME-focused accounting and advisory firms must surely have a point of saturation when the demand to acquire practices will decrease or dry up, and the valuations available will recede accordingly. It is, of course, up to the motivations of the existing business owners as to whether to seek participation in the present trend or to maintain a focus on businesses owned and managed by talented professionals who work in them. Either way, the implications for those working in those businesses are likely profound.

Is it over for the independent firm? Big players in the industry have traditionally always spun out entrepreneurial professionals who see the opportunity to own their own businesses and do it “their way”. Some observers believe that present trends will sustain (or increase) this talent spinoff phenomenon. Meanwhile, the costs and other barriers to accessing technology and other business facilitators progressively decrease, increasing the potential for start-ups and smaller businesses.

The landscape may be shifting as the second division reorganizes itself. There will likely be a high point in valuations and disposal opportunities, and that could potentially be close. But it may well be a mistake to assume that the days are gone of the independent firm owned and managed by the talented professionals working within it.

Epilogue – The Prelude Corporation

In AGN high potential talent training programs, we sometimes refer to the Harvard Business Review classic 1970s case study The Prelude Corporation. It tells the story of where “Big Business” tried to modernize, systemize and defragment the lobster fishing industry in New England USA.

Whilst the case clearly has some age, it remains a relevant and cautionary tale. Big Business failed in its objectives, and the business became unviable. Why? At the end of the case study, we share the following elucidatory quotation:

“You don’t make lobster; you hunt them. Your success depends on the flare, skills and initiative of people who can’t be effectively supervised. The product of people who feel genuine commitment, who have acquired from the rest of the crew an understanding of and devotion to excellence in lobster fishing.“

The point is that performance in the lobster fishing industry depends on the skills and experience of engaged and motivated professionals. They regarded themselves as hunters, not factory operatives – a “craft” if you will? They did not care to be supervised and systemized but craved autonomy to approach the task as they saw fit and their experience demanded.

It is not hard to draw parallels between our own industry and the present trends and changes that we have discussed above. Of course, much has changed in 50 years. But have the fundamental motivations of people? Or have other things changed sufficiently so that these pitfalls can be avoided? Perhaps so, but possibly not. We will see.

News just in…

It’s reported that Apollo Global Management has entered into an agreement involving a $1.3 billion debt deal with the accounting firm BDO USA. Apparently, the funds will be deployed to secure a minority ownership interest in the company from its existing partners. BDO recently converted its 860 partners into employee shareholders of a corporation. Within this framework, the ownership of BDO USA will remain in the hands of its workforce, as ownership is set to be apportioned among the partners and a tax-efficient retirement savings mechanism known as an employee stock ownership plan (ESOP).

Want to go further?

AGN can offer members bespoke researched and facilitated strategy workshops on realizing value, migration to advisory services or operational

effectiveness (amongst other topics). There can be genuine benefits in gathering the partner group away from client and staff demands for a few hours and using AGN to help the team come together in defining a future strategy. If you would like to discuss these options, please contact Malcolm Ward, AGN Global CEO [email protected].

Appendix 1: The value key challenge – what might an investor look for?

The Value Key is an indicator of where management might most effectively apply their energy and resources, but it is also a lens through which to consider the business from the perspective of a prospective investor or buyer. Click here to download Appendix 1.

| Value Key Element | Organizing Value to Appeal to an Investor | Investor View |

|---|---|---|

| Vision, Direction and Communication | Action: Ensure that there is a clear strategy and goal in the mind of the staff. Encourage the teams to consider the ‘values’ of the business in terms of day-to-day execution. | High levels of staff work satisfaction are linked to clear and achievable strategies and goals. Encourage the physical manifestation of the firm’s values and ethos through iconography, staff ‘owned’ initiatives, high internal and client satisfaction scores, and evidence that the team understand ‘the plan’ and supports it. All of which indicates to an investor an engaged, dedicated workforce. |

| Operational Effectiveness and Technical Excellence | Action: Establish an Operations Manual that documents critical business processes, financial controls, employment policies, complaint procedures, and client take-on procedures – map every critical process in the business and assign responsibility in the business for the maintenance of each. | The record of process and policy produces clarity and efficiency in running the business and (if relevant) can also facilitate the ‘discovery’ process for the investor. With someone attached to each key process, the investor will have the comfort that they won’t be left stranded if there’s a breakdown in a system. |

| Growth & Business Development | Action: Put in place a 3-to-5-year strategic marketing plan detailing the future trajectory of business growth. Set out niche and specialist developments, both existing and future ideas and potential investments. This should help you focus on investment and development to maximize future potential and performance. (Refer to AGN 6 Star Business Development Model at My AGN / AGN Solutions (or My Resources) / Business Strategy & Growth. | Indicates to an investor how you are aligning the business for future growth and expansion. This speaks to the idea that you are effectively selling the future of the business, not its past. |

| Best Clients | Action: Put in place an annual approach to Key Account Management, ensuring that you genuinely achieve whole-business commitment to the longevity and maximizing value of each key client relationship you identify. Share-of-wallet and likely cost recovery can be increased, and potential change points and succession issues can be identified and planned for. (See AGN Guide to Key Account Management). | Generally considered to be a significantly more effective performance driver than new client acquisition, “sticky” well-managed key clients will contribute directly to investors’ perception of value. |

| Innovation & Technology | Action: Create a 3-to-5-year strategic technology plan to be woven into your annual financial and operational budgets. Document where you are on the path to digital transformation, map out software upgrade paths and digitization of processes, and the impact of service offerings. Ensure you have a talented and knowledgeable ‘Tech Champion’ among your senior team who is responsible for running the project into the future (after you have left the business). | Incoming investors might have their own ideas and plans in this area, but understanding that the business has a coherent existing approach will contribute to value. |

| Talent Leadership | Action: Create a 3-to-5-year strategic talent plan – what are the resources and skills you’ll need for the future, and how do you plan to ensure their availability? A key part of this must be succession planning, not only in terms of equity ownership but also for the other key leadership positions and commercial drivers in the business (See AGN Succession Strength Guide). Consider modelling your talent pool, for example, using the 9-box model, considering potential and performance alongside longevity. What are your plans for succession in the business? To achieve value, it is necessary to focus on individuals with the underlying talent and aptitude, as well as the development of commercial and softer skills needed to run a business for profit. | An effective plan will help assure business resilience and longevity and provide a clear path to retain and develop in-house talent, all of which will contribute to internal and external judgements of value. |

Copyright © 2023 AGN International Ltd. All rights reserved. No part of this publication may be reproduced, distributed, or transmitted by non-members without prior permission of AGN International Ltd.